Have you ever done this: before buying a laptop, you check the CPU, the memory, the cooling system—and even spend three hours on PTT forums confirming the machine won’t have problems.

Before buying a NT$200 chicken cutlet, you check Google reviews to confirm the shop hasn’t been busted for using recycled oil.

But think about it: when you put hundreds of thousands or even your entire one or two years’ salary into a stock, where did that super-picky, super-smart, super-risk-averse you go?

Suddenly you become extremely generous—you stop checking specs, quality, or price.

What are you looking at? A coworker’s offhand lunch comment: “Hey, I heard that stock is good.” A line of small text under a news ticker. Or worse—you see the K-line rising, get that FOMO feeling “if I don’t get on now it’ll be too late,” and then throw your money in.

That’s not investing. That’s crossing the road with your eyes closed—while holding your family’s hand.

Today I won’t talk about debits, credits, or accounting entries. Leave those headaches for accountants. What we’re going to do is simple: bring back that fussy, picky, price-sensitive brain you used when buying a laptop.

Buying a laptop, you only need to check three core specs. The same goes for stocks—you only need to confirm three numbers. In just 3 minutes, you can avoid the roughest, deadliest, easiest-to-fall-into landmines on the market.

You don’t need to read hundreds of pages of annual reports, you don’t need to listen to advisors spinning stories, you don’t even need to understand macro or chip patterns—this 3 minutes will protect 99% of your principal.

1. Your First Investment Goal: Don’t Lose Money

Before explaining these three numbers, I need to nail one thing into your brain.

Do you know why many people invest their whole lives, only to find when they tally up they’ve not only made nothing but lost a big chunk of their principal? Because they got the most basic, most important, and most easily overlooked order wrong—the first goal of investing isn’t to make money, the first goal is to not lose big.

The Buffett quote that’s been quoted to death but should be taken seriously every time you hear it: “Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1.”

Many people hear this and think it’s obvious—who wants to lose money? But do you really know the weight of these words?

Let’s grab a calculator:

- If your assets drop 50%, how much do they need to rise to get back? Not 50%—100% (double).

- What about a 90% drop? You need a 900% gain to get back to where you started.

Going down is taking the elevator down, but breaking even is rock climbing without ropes.

One big loss doesn’t just cost you a bit of profit—it directly destroys the next 3 to 5 years of your investment rhythm. This is how many people work: panic-selling during the 2020 pandemic crash, watching the index climb all the way back up, and by the time they finally muster the courage to re-enter, others are already preparing to take profits.

This is why the people who truly last in the market aren’t just hunters chasing targets—they’re engineers who know how to avoid landmines. Benjamin Graham, the father of value investing, said it clearly: “Investment is thorough analysis to ensure the safety of principal and obtain a reasonable return.” Note the order—safety first, return second.

The three numbers we’re learning today are three landmine-clearing tools. Not digging desperately for a diamond in a trash heap—but first clearing the most obvious, most dangerous trash.

2. Number One: ROE (Return on Equity)

Sounds technical, right? Return on equity. Just remember one concept: how much profit this company makes from shareholders’ money.

Imagine two chicken cutlet shops you could invest in:

- Owner A: Spent NT$10 million to open a top-tier shop with imported fryers and max AC—made NT$1 million in a year.

- Owner B: Spent NT$1 million on a roadside stall with a cart and an umbrella—also made NT$1 million in a year.

Who do you give your money to?

Owner A used NT$10 million to make NT$1 million = 10% return. Owner B used NT$1 million to make NT$1 million = 100% return. In this simplified example, the efficiency differs by 10x.

If Owner B can scale up at the same efficiency, the profit imagination is in a completely different league.

This is retail investors’ most common mistake—looking only at absolute numbers. TSMC makes hundreds of billions a year—sure, it’s a good company. But for you as a small shareholder, what matters isn’t how much TSMC earns—it’s what proportion of return it earns on your money.

You buy a stock by handing your hard-earned money to a company to operate. What you should care about is efficiency. Why does Buffett value ROE so highly long-term? Because companies with high ROE, if they can steadily reinvest profits, can earn more and more without constantly asking shareholders for more capital—they grow like a snowball.

Conversely, if a company’s ROE is chronically lower than the risk-free rate, what right does it have to ask you to bear stock risk? You put money in a time deposit and earn interest steadily. Then you buy this company’s stock, the price keeps you up at night, and in the end your efficiency is even worse—that company is just consuming your patience and capital.

The Hidden Trap of ROE

Of course, mature manufacturing ROE varies greatly with the industry cycle—you can’t use one yardstick for every company. But if a company maintains ROE above 15% for three consecutive years, you can at least say this boss runs a decent business.

But here’s a very hidden trap—the formula for ROE has “shareholders’ equity” in the denominator. Remember fractions from elementary school? To make a fraction bigger, you can make the numerator bigger or make the denominator smaller.

Bad operators manipulate the denominator:

- A company loses money for several years, shareholders’ equity gets eaten down to almost nothing. Suddenly one year the cycle rebounds and they make a small profit—because the denominator is tiny, ROE can spike to 50% or 60%

- A struggling company sells its last piece of land, dumps a one-time gain in, and ROE instantly jumps

You see these numbers and think you found a treasure, rush in—and end up buying the last firework.

So one year’s number isn’t enough—look at three years. Three consecutive years of stable 10-15% or more, not propped up by asset sales or one-time gains—that’s closer to the real deal.

It’s hard to hit home runs three years in a row by luck. With these companies, even if the stock price dips, you won’t panic as much because you know their factory is still making money, cash flow is still coming in.

3. Number Two: Debt Ratio (Debt to Equity)

First checkpoint: can the company make money. But making money doesn’t mean it won’t go bankrupt—which brings us to number two: debt ratio.

Have you heard the term “black-text bankruptcy”? That means the books show profits but the company still can’t maintain cash flow and goes under. Why? Maybe customers haven’t paid, maybe interest pressure is too high, maybe the bank won’t roll over short-term debt.

A mountain of debt just needs a small storm to come crashing down.

Use the laptop analogy: it’s like a laptop with crazy performance—but the shell is made of glass. Boots super fast, but one drop and it shatters. Would you bet everything on that laptop?

In good times, these companies look fine. Low interest rates, banks willing to lend, they use other people’s money to grow their scale, ROE looks great—the ROE I mentioned earlier sometimes gets inflated by over-leverage.

But the economy can’t be summer forever. When winter comes, rates rise, banks start pulling in credit lines, these companies immediately suffer—their earnings get eaten up by interest. Severely, even if the core business is still profitable, the capital chain can snap and they collapse in an instant.

In the 1997 Asian Financial Crisis, how many companies didn’t disappear because their products vanished overnight—but because their leverage was too high, foreign currency debt too heavy, capital chain too fragile? One dollar of their own money, several dollars borrowed; exchange rate moves, rates rise, they’re drained dry.

Safe Levels of Debt Ratio

How much debt-to-equity is safe? A simple initial screening:

| Debt / Equity | Risk Level |

|---|---|

| Below 80% | Safe zone (comfortable for non-financial industries) |

| Below 150% | OK, at least has a safety belt |

| Above 280% | Yellow light (unless aviation, shipping, finance, utilities) |

| Above 400% | High risk zone, bomb at your feet |

Like ROE, watch the trend—if the debt ratio crawls from 100% to 200%, the company may be deteriorating. Conversely, going from 200% down to 100% suggests improvement. The latter is sometimes more worth your research time.

4. Number Three: P/E Ratio

Checkpoint one: makes money. Checkpoint two: doesn’t go bankrupt. Checkpoint three: is the price reasonable.

The third number is the P/E ratio. With a rough analogy: how many years would it take to recover your investment through earnings, assuming zero growth.

Say you spend NT$1 million buying your friend’s coffee shop. Looking at the books, it makes NT$100,000 a year. How many years to break even? Ten years. P/E is 10. Same with stocks: a company with NT$10 billion market cap earning NT$1 billion a year has P/E of 10. With current earnings speed and no future growth, 10 years to break even. P/E of 100? 100 years to break even—you probably won’t live that long.

So Is Lower P/E Always Better?

On the surface, yes—lower means faster break-even at current earnings. Many books teach you to find low P/E stocks, finding ones at 4x or 5x like striking gold.

But here’s a big trap. Today you see the latest laptop model online selling for only NT$15,000. Would you immediately buy? No—you’d suspect it’s broken, fake, or has a dead screen.

In the stock market, stocks with absurdly low P/E often signal that the market doesn’t believe the company can maintain current earnings. Sunset industries are the classic example—the company is still making money, but over the next 10 years demand is declining, policies are headwinds, costs are rising. The market doesn’t believe in its long-term earnings, so the price gets crushed.

You think you found a bargain, but what you bought was a ticket on a sinking ship—just a cheaper ticket. This is called a value trap.

Conversely, there are companies with P/E of 100, 200, or even higher. Tesla at its most euphoric phase had absurdly high P/E. Using the coffee shop analogy: you spend NT$1 million on a shop making only a few thousand a year—crazy, right? But why does everyone line up? Because they’re not betting on current earnings, but on potential future growth explosions.

So How Do You Judge?

Simple answer: compare. Don’t draw conclusions from one number.

P/E is relative. Does it make sense to compare a sumo wrestler’s weight to a marathon runner’s? Sumo at 150kg is normal, marathon at 60kg is normal.

Same with stocks—compare manufacturers to manufacturers, tech to tech. Go to your broker’s app, find the company’s peers, check what their average P/E is:

- If your stock has P/E of 5 but peers average 15, ask why this one is so cheap. Bad news? Earnings declining? Or just being ignored?

- If after checking you find no obvious issues, then there’s room to discuss undervaluation.

Conversely, if your stock has P/E of 50 but peers average 10, calmly ask yourself: is it really 5x better than peers? Can future growth really support this price? If you can’t answer, what you’re buying may not be a dream—but a bubble.

5. Where These Three Numbers Don’t Apply: Biotech and Platform Companies

But I have to be very responsible and tell you: these three numbers can’t be applied with the same yardstick on certain companies.

The most typical example is biotech. You’re the boss of a new drug company. Developing a new drug may take ten years and burn through tens of billions. If successful, it brings huge licensing fees and sales—but the problem is it’s still in R&D, burning cash every year.

How does the financial report look? Annual losses, P/E can’t be calculated, ROE is negative, debt may look terrible. By the numbers, this company should go bankrupt immediately—but it may not be burning money meaninglessly. It may be betting on a product line, a patent, a clinical trial result.

If you buy biotech stocks and only use P/E to complain they’re too high, it’s like going to a football field and complaining why you can’t use your hands—the rules of the game are completely different.

Platform companies are the same. E-commerce, delivery, ride-hailing platforms often burn through cash heavily in early stages—not because they can’t make money, but because they choose not to first, throwing money into logistics, user subsidies, market share grabs, with the goal of building scale and network effects. Asking these companies to deliver profit now is like telling a general at war to go back and farm.

At this point you should look at revenue growth speed, market share, unit economics, and whether they can survive once subsidies end—not P/E.

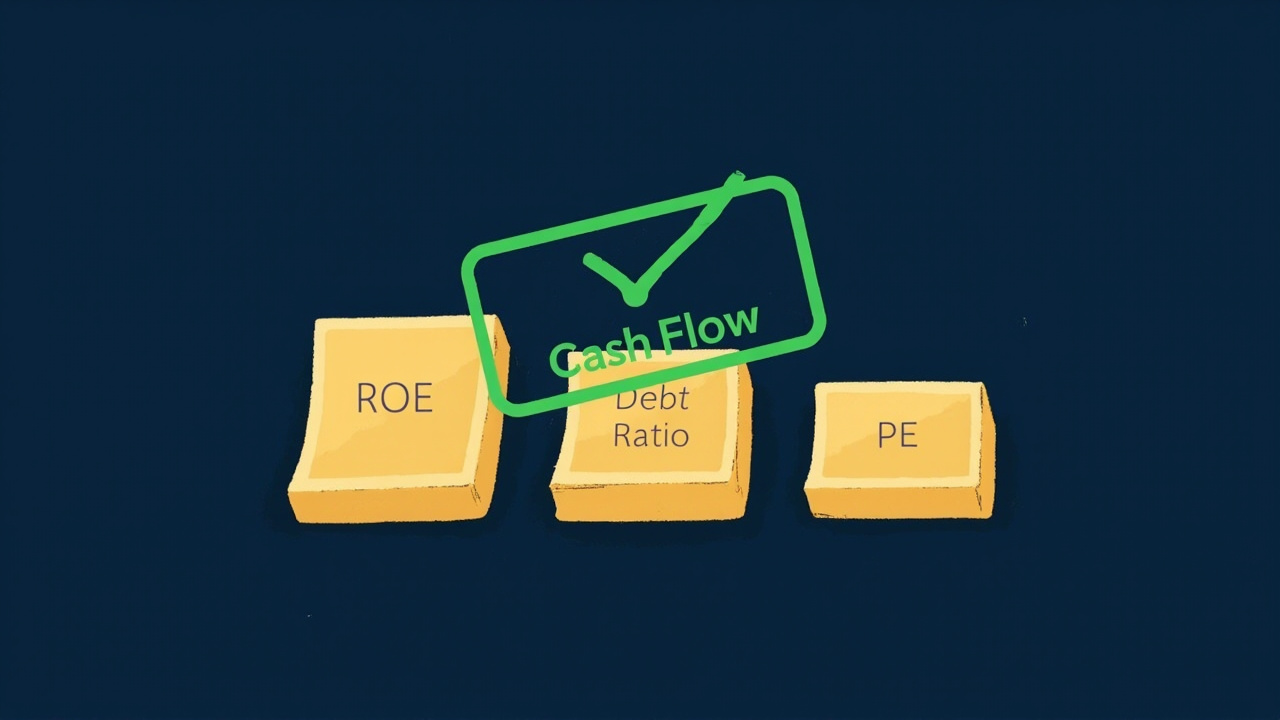

6. Advanced Tool: Operating Cash Flow

Beyond the three numbers, I’ll give you one more tool—an advanced one that real experts seriously look at.

ROE and P/E are both based on “net income,” but accounting has a fatal weakness: net income is a book number—it doesn’t necessarily equal the cash that actually hits your bank account.

- Customers buy on credit—the books recognize revenue and profit, but the cash hasn’t come in.

- Warehouses are stuffed with unsold inventory—it may still be on the books as an asset, but whether it can actually be sold is another matter.

Shrewd operators exploit this to make the books look great—paper profits, but cash gets tighter and tighter, eventually leading to cash flow trouble—this is the most common path to the “black-text bankruptcy” I mentioned earlier.

So real experts look at something called “operating cash flow.” The name sounds long, but the meaning is simple: regardless of how the books are written, how much cash did this company’s core business actually generate?

There’s a saying I want you to memorize: “Profit is opinion, cash is fact.”

Accounting can dress up profit nicely, but the cash flow statement at least lets you see whether the business is actually collecting cash. Of course, cash flow can also be manipulated to some extent, so you need to look at it together with accounts receivable, inventory, and notes in the financial statements.

Here are two simple judgments:

- Net income is positive but operating cash flow is negative for several consecutive quarters—red flag. This means things may have been sold but money not collected, or inventory piling up—looks shiny on the surface, but bleeding internally.

- Net income is negative but operating cash flow is positive—this one is sometimes worth a second look. Could be depreciation and amortization making the books look like a loss, but cash still coming in. This kind of company may not be great, but it has research value. When others see the financial reports look bad and throw them away, those who understand cash flow have a chance to pick up pearls at the bottom.

7. The Hardest Thing Was Never the Numbers—It’s Your Brain

Alright, the numbers are done. But let me tell you honestly—do you think the hardest part of investing is learning to read numbers?

No. It’s not the market, not technical analysis, not macro judgment. The hardest part is your brain.

Your brain evolved over millions of years of hunting and gathering. Back then, the survival rules were simple: if someone runs, you run; if there’s movement in the grass, flee first; absolutely don’t let food be taken from your hands. These instincts, in the stock market, often become fatal bugs.

The Most Severe: Loss Aversion

Behavioral economics research shows that humans feel about twice as much pain from a loss as pleasure from an equivalent gain.

What tragedy does this cause in investing? Your account has two stocks: A is up 20%, B is down 20%. You need to sell one. Which do you sell? Most people sell A first. Why? You want to lock in the pleasure of profit, you don’t want to face the pain of loss. So you hold B, hoping it comes back.

What’s the result? You cut the blooming plant and keep the ugly weed. Your account is eventually full of stuck, rotten stocks. It’s like a gardener cutting the roses and seriously watering the weeds.

Another Fatal Bug: Herd Mentality

Your neighbor Wang bought a stock and got a new car—your stomach starts hurting. Everyone’s lining up to grab something and you want to squeeze in too—who cares if P/E is 100x or debt 500%, just buy first. Then you buy at the mountaintop, sell at the bottom after the crash—because everyone’s fleeing and your instincts say you should too.

Buy high, sell low, again and again, forever harvested.

How to Beat Your Instincts?

Willpower isn’t enough—willpower is like a muscle that runs out. A more reliable method is to build a system that doesn’t let emotions directly control your account.

Why do some professional investors survive long-term? Not necessarily because they’re smarter every time, but because they have rules, risk control, and discipline.

- When things rise too much, they mechanically check valuations

- When things fall too deep, they recheck fundamentals

- When retail investors are greedy, they at least know to ask “where’s the risk?”

- When retail investors panic, they at least know to ask “is the value still there?”

If you can’t figure out this structure, you’ll easily become the market’s ATM. Investing isn’t an IQ war—it’s more of an emotional control and risk management war.

8. Put These 4 Numbers Into Muscle Memory

So today you’ve learned three numbers plus one advanced tool:

- ROE: profitability efficiency

- Debt-to-equity ratio: can it be crushed by debt

- P/E ratio: is the price reasonable

- Operating cash flow: lie detector

You can check all four in 3 minutes. Next time someone gives you a hot tip saying some stock will rise, don’t rush—open your broker app and check these four numbers. In 10 seconds you’ll know whether to keep listening.

There’s no one-size-fits-all secret to investing—even if there were, you shouldn’t take it as gospel. But there are ways to reduce your risk of overnight bankruptcy, and that’s what we covered today.

Starting today, every time you want to press “buy,” spend 3 minutes first. These 3 minutes will protect your money better than any hot tip, any insider info, any gut feeling.

9. Behind Discipline is Respect

Finally, I want to share something deeper. Have you noticed that on the surface we’re talking about stocks, numbers, and financial ratios—but underneath the logic is really two words: discipline.

And behind discipline are two more words: respect.

Respect your money.

Do you know where your money comes from? It’s from waking up early every day, riding the bus, getting yelled at by your boss, working overtime late into the night, sacrificing time eating with family, giving up things you wanted to buy—one drop at a time.

Every dollar is your time. Every dollar is your freedom. When you casually throw it into something you don’t understand, you’re not investing—you’re abandoning your past.

You think you’re just buying a stock—no, you’re handing a small piece of your life to someone else.

So when you start taking these three numbers seriously, when you start being willing to spend 3 minutes doing homework, you’re not becoming better at investing—you’re showing respect for the time you’ve spent in the past.

Ten or twenty years from now, you’ll find the gap between you and others isn’t wealth—it’s the gap in choice.

When others panic at a market storm, sell at the bottom, and see their life plans collapse—you, because you know what you bought, know your companies are still making money, know the price fell but the value didn’t disappear, can sit there steadily, even have room to buy more at better prices while others are fearful.

When others at 50 or 60 are still anxious about whether their retirement savings are enough, still watching the market daily, still being pulled by market emotions—you already have enough assets generating cash flow to cover your basics. You don’t need to read your boss’s face anymore, you don’t need to tolerate things you hate for a salary.

That’s not financial freedom—that’s life agency.

The 3 minutes you spend today aren’t about learning three numbers—they’re about buying yourself a little more choice 10 or 20 years from now.

You don’t need to be amazing, you don’t need a lot of money, you don’t need to wait—you can start today.

Starting today, spend 3 minutes before every buy. Just this one action repeated a thousand times, and your future will thank your present self.

This article is for personal experience sharing only and does not constitute any investment advice, buy/sell recommendation, or profit guarantee. All investing carries risk; please make independent judgments based on your own financial situation and risk tolerance.

Comments