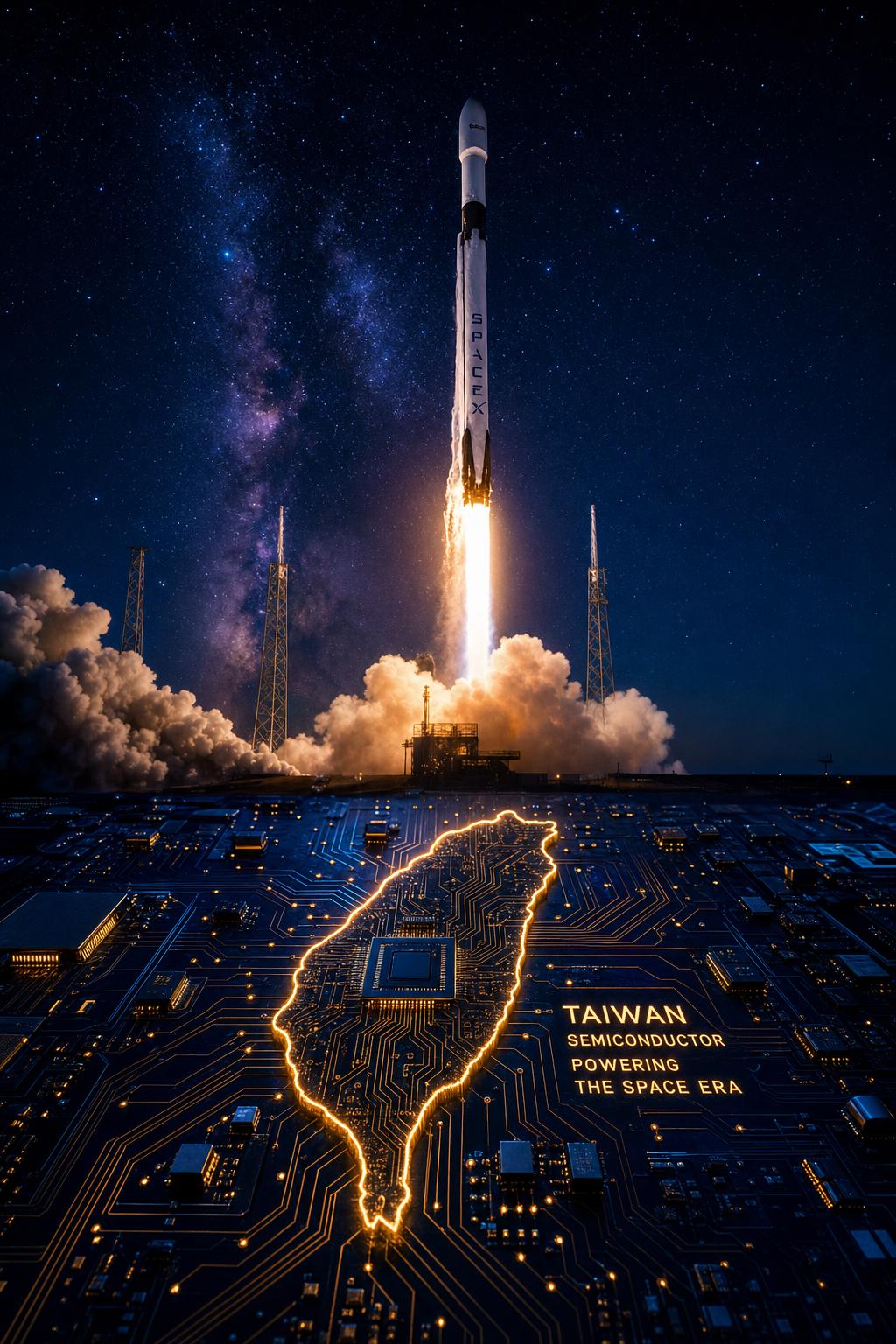

On June 12, 2026, global capital markets witnessed the largest IPO in history: SpaceX officially listed on Nasdaq under the ticker SPCX, priced at 75 billion** and reaching a valuation of $1.77 trillion — surpassing most tech giants.

The moment news broke, Taiwan’s stock market felt the impact. Investors scrambled to search: “Which Taiwan stocks benefit from SpaceX?” and “Is it too late to buy Ascend Science?” Behind these questions lies a more fundamental wealth question: When a sector theme transitions from narrative-driven speculation to fundamental earnings delivery, are you positioned for it?

This article gives you a complete breakdown of Taiwan’s SpaceX proxy stocks — categories, purity levels, risks, and most importantly: the investment logic behind them.

Why SpaceX’s IPO Matters Far Beyond a Single Listing

SpaceX is no longer just a rocket company. By 2026, its commercial empire spans three vertically integrated segments:

- Starlink: Low-earth orbit satellite internet, projected to contribute over 80% of total revenue in 2026 — SpaceX’s primary cash engine

- Starship commercialization: Heavy-lift launch vehicle entering commercial markets, with per-launch costs continuing to decline

- Space AI Data Centers: In May 2026, SpaceX announced a collaboration with Anthropic to develop orbital computing infrastructure, dubbed “AI cloud in orbit” by markets

All three business lines share one characteristic: extreme hardware dependency, and deep reliance on Taiwan manufacturing.

Every Starlink satellite batch requires thousands of high-frequency PCB boards, RF components, antenna modules, and power supplies. Ground station expansion equally drives demand for routers and communication modules. Crucially, SpaceX quietly sent a team to Taiwan in early 2026, specifically targeting Ascend Science (3491) and Unimicron (2313) — with the goal of expanding orders and sourcing new Taiwanese partners to meet next-generation satellite upgrade requirements. This “customer knocking on your door” signal is extraordinarily rare in electronics supply chains, confirming Taiwan’s role not as bystander but as critical infrastructure provider in the space revolution.

Taiwan Stock Categories: Supply Chain Purity Determines Your Return Potential

The market labels 30–40 Taiwan stocks as “SpaceX proxies,” but purity levels vary dramatically. First, understand which category you’re buying.

Category 1: Direct Core Suppliers (Highest Purity)

These companies ship products directly to SpaceX, hold space-grade certifications, and have confirmed supply relationships via public filings or earnings calls.

- Ascend Science / Unictron (3491): Widely considered Taiwan’s highest-purity satellite stock. Specializes in high-frequency microwave filters, duplexers, and OMT components. Satellite revenue reached approximately 80% of total revenue in Q1 2026, with gross margins consistently above 60%. One of SpaceX’s primary visit targets when they toured Taiwan, with a decade-long supply relationship spanning ground stations to satellite payload systems.

- Unimicron (2313): World’s largest low-earth orbit satellite PCB manufacturer. Holds approximately 90% global market share for Starlink satellite body boards — extremely high technical barriers, minimal substitutability. Expanding capacity in Thailand; analysts estimate 2027 EPS of NT$12.37, up over 60% year-over-year.

- Wistron NeWeb (6285): Core assembler of Starlink user terminals (UT) and satellite routers. Produces Starlink routers in Vietnam. One of three Taiwan companies specifically named by Reuters as confirmed SpaceX suppliers.

- Meccatronical Energy (6443) / Yuanching: Taiwan’s only company in SpaceX’s solar energy supply chain, shipping satellite solar cell modules since 2022.

Category 2: RF & Packaging Materials (High Technical Moat)

- WIN Semiconductors (3105): World’s largest gallium arsenide (GaAs) foundry. Early entrant into SpaceX’s inter-satellite high-frequency links and D2C (direct-to-cell) technology. Satellite products expected to make first meaningful profit contribution in 2026.

- Tong Hsing (6271): High-frequency ceramic-package RF transceiver modules. Market rumor suggests exclusive packaging supply for specific SpaceX satellite frequency bands. Low profile but deep technical moat.

- Taiflex (2383) / Wah Hong (2367): High-frequency copper clad laminate (CCL) for satellite bodies and ground stations — critical upstream materials for PCB manufacturers like Unimicron.

Category 3: Ground Equipment & Power Systems (Broad Beneficiaries)

- Delta Electronics (2308): High-efficiency power supply units (PSUs) with 96%+ conversion efficiency for Starlink ground stations and future orbital data centers. Stock up over 85% since the start of 2026.

- Auras Technology (3017) / Shuang Hong (3324): Thermal management specialists. As SpaceX expands “Space AI computing” demand, their liquid cooling technology gains further market attention.

- Innolux (3481): Pivoting with FOPLP (Fan-Out Panel-Level Packaging) technology into SpaceX RF chip packaging — a “theme transformation dark horse” transitioning from display panels to semiconductor packaging.

Category 4: ETF — The Smart Lazy Approach

For investors who prefer not to pick individual stocks, the First Capital Space Satellite ETF (00910) holds Ascend Science, Unimicron, Wistron NeWeb, and other core Taiwan SpaceX supply chain players. Year-to-date returns have exceeded 67%, making it a solid core-satellite allocation for satellite sector exposure.

4 Stock Selection Criteria: Avoiding the “Fake Proxy” Trap

The market is flooded with “SpaceX proxy” labels, but many are peripheral theme plays with minimal actual order contributions. These 4 criteria help you filter quickly:

1. Satellite Revenue Percentage The proportion of space/satellite-related revenue to total revenue reflects purity. Ascend Science is approximately 80%; Unimicron’s satellite board segment is its biggest growth engine. If a company’s space revenue is only 5%, even the loudest theme label barely moves the EPS needle.

2. Space-Grade Certification Barriers Aerospace-grade component certification cycles span years, and once in the supply chain, customer stickiness is extremely high. Companies with space certification (Ascend Science, Yuanching, etc.) possess the strongest moats — substitution is nearly impossible.

3. Multi-Customer Diversification (Not Just SpaceX) Amazon Kuiper, OneWeb, and Telesat are all expanding rapidly. Ascend Science already supplies both SpaceX and Amazon Kuiper. Companies capable of serving multiple global satellite operators have more durable growth momentum.

4. Earnings Call & Financial Report Confirmation Theme speculation often pushes prices up before actual results arrive. If subsequent earnings fail to confirm, it becomes a textbook “buy the dream, sell the reality” trap. Before buying, verify: has management explicitly disclosed satellite order volumes and forward visibility in earnings calls?

Post-IPO Investment Logic: From Theme to Fundamentals

After SpaceX officially listed, the most common investor trap is: “I missed it before the IPO, so chasing it now is pointless.” This logic overlooks one key reality: theme ignition is just the starting gun — fundamental order delivery is the fuel for the main upward move.

SpaceX plans to launch over 5,100 satellites in 2026. The V3 Starlink satellite carries 10x the communications capacity of prior generations, meaning high-end PCB specifications are upgrading across the board and high-frequency microwave component demand is multiplying. This isn’t a one-time theme consumption event — it’s a sustained order growth cycle from 2026 through 2029.

Key catalysts to watch for market timing:

- V3 satellite mass production shipment timeline: Each batch of shipments directly triggers PCB and RF component order volumes — the most immediate stock price catalyst

- SpaceX Direct-to-Cell (D2C) service expansion: Drives long-tail demand for WIN Semiconductors, Ascend Science, and related RF companies

- Space AI Data Center progress: If the Anthropic collaboration materializes, the thesis for Auras Technology, Shuang Hong, and other thermal management companies strengthens further

- Taiwan supply chain non-China capacity investments: SpaceX requires suppliers to mitigate geopolitical risk; Unimicron’s Thailand expansion and Wistron NeWeb’s Vietnam factory ramp directly affect order fulfillment capacity

The biggest beneficiaries of this space revolution are not day traders staring at tick charts, but long-term investors who can identify industry cycles, quietly build positions before themes ignite, and smile holding through fundamental delivery. Taiwan’s PCB, RF components, and thermal technologies are literally orbiting Earth right now — and that fact carries far more weight than any single limit-up day.

Information about individual stocks mentioned in this article is for reference purposes only and does not constitute investment advice or recommendations. Stock investing involves risk; past performance does not guarantee future returns. Investors should conduct their own due diligence and make investment decisions based on their individual risk tolerance.

Comments